London, 6 August 2025 – Canopius Group, a leading international specialty and P&C (re)insurer, today announced its financial results for the half-year ended 30 June, 2025.

Key highlights include:

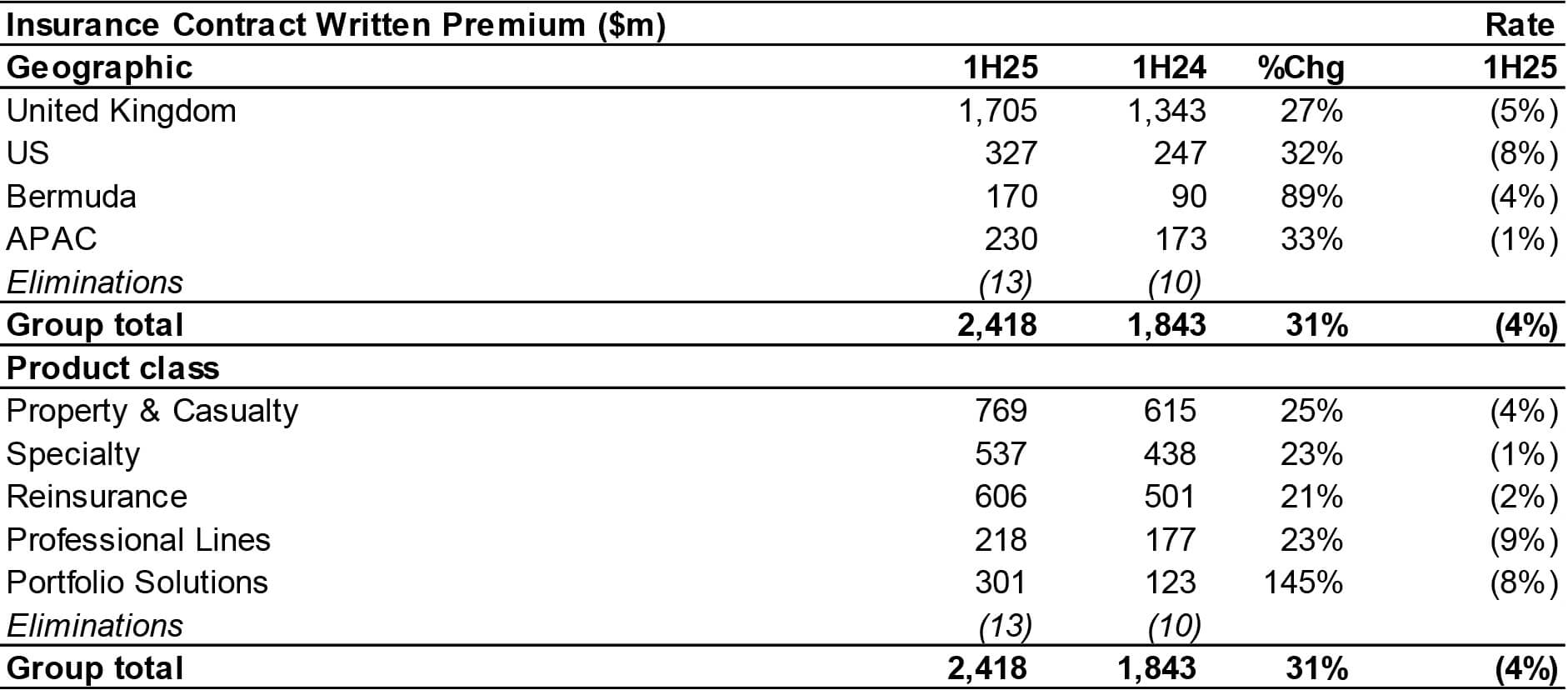

- Insurance Contract Written Premium increased 31% to $2.41bn (1H24: $1.84bn)

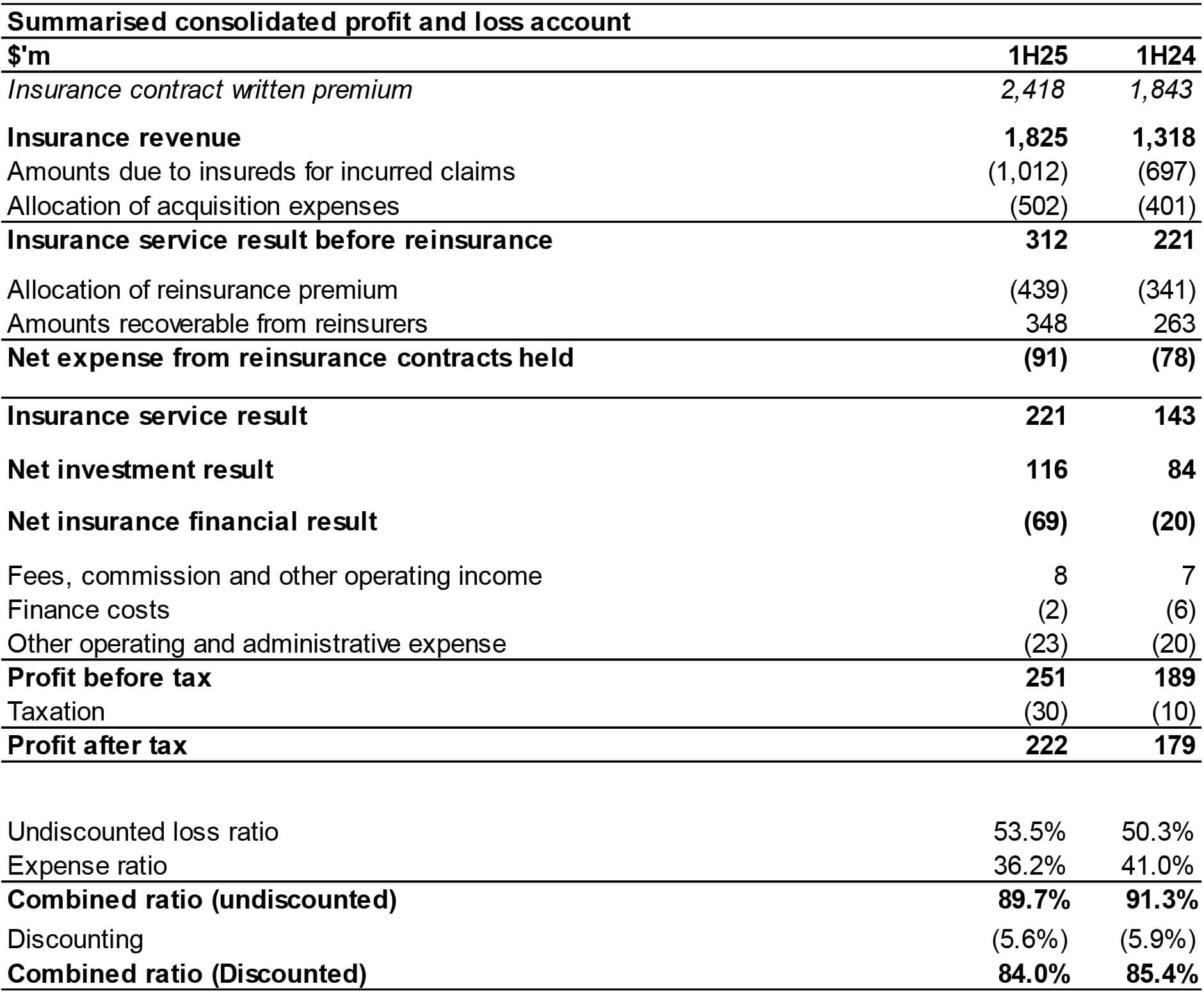

- Net insurance revenue increased 42% to $1.39bn (1H24: $0.98bn)

- Group net combined ratio (undiscounted) of 89.7% (1H24: 91.3%)

- Group net combined ratio (discounted) of 84.0% (1H24: 85.4%)

- Profit after tax increased 24% to $222m (1H24: $179m)

- Tangible Net Asset Value (TNAV) increased to $2.04bn (YE 2024: $1.81bn)

- Annualised Return on Opening Tangible Equity (ROTE) of 24.5% (1H24: 23.9%)

Neil Robertson, Group Chief Executive Officer, said:

“At Canopius, we are guided by a clear strategic vision focused on delivering attractive, sustainable returns by expanding in areas where we have a competitive edge or differentiated capabilities. Our relentless focus on underwriting and execution has created strong business momentum that has again allowed us to deliver both attractive growth rates and robust underwriting profitability.

The Group is well placed to capitalise on the strong fundamentals of our industry. The ongoing enhancement of our operational capabilities combined with our disciplined underwriting approach continues to position us well to take further advantage of emerging opportunities and sustain our profitable growth.”

Continued momentum in top-line and bottom-line performance

“The year has started well. Despite rate pressure emerging across parts of our portfolio, the breadth of our business and the momentum we have generated in recent periods has been reflected in material premium growth at strong levels of rate adequacy. We were again able to demonstrate growth and profitability across our business regions in the UK, US, Bermuda, and APAC.

The California wildfires in January were a significant though not outsized event for Canopius, but there were many smaller catastrophe events during the period, and this led to higher catastrophe losses relative to the prior half year. However, attritional loss experience is stable, with positive reserve experience on both current and prior years.

Our balance sheet has strengthened once again this half year. The investment return from our high-quality investment portfolio continues to trend positively as our business grows and we continue to maintain a prudent reserving position and have a robust capital surplus.”

Focusing on the enhancement of our value proposition

“To deliver lasting value to our customers and shareholders, we remain committed to driving excellence and consistency across our business. In recent years, we’ve accelerated our progress, building a more diverse and resilient enterprise through the disciplined execution of our strategic priorities.

“As market competition intensifies, we continue to apply a disciplined and selective approach to capital allocation with a strongly held commitment to pricing integrity across all parts of the Canopius Group. We are confident in our ability to navigate the remainder of 2025 and to further enhance our value proposition.”

Note: Unless otherwise stated, all figures are on IFRS 17 basis. Numbers in tables may not add up due to rounding.

Group 1H 2025 Financial Results commentary

CEO’s statement

Strong revenue growth, lower expense ratios and a higher investment return were the primary drivers of the uplift in profit against the prior period.

Our underwriters remain focused on delivering profitable growth and Canopius has maintained its strong momentum of recent periods, notwithstanding emerging rate pressure in selected product areas. Attractive organic growth has been recorded across both product categories and geographic regions whilst maintaining our underwriting discipline.

The modest increase in our undiscounted loss ratio during the period reflects elevated industry-wide catastrophe activity during the first half of 2025. Importantly, attritional loss ratios remained stable, despite absorbing several significant market events, including the aviation leasing legal judgment and several large losses in the Energy sector. Favourable development on both current and prior accident years continues to demonstrate the prudence of our reserving approach.

Changes in business mix during the period contributed to a reduction in acquisition costs. In parallel, our disciplined approach to expense management, supported by top-line growth, is creating operating leverage and yielding improvements in our administrative expense ratio as we scale the business.

Investment returns experienced significant growth over the previous year, primarily due to high-quality recurring income generated from our expanding asset base. While some fair value gains were recorded, these were largely offset within insurance finance expenses due to our asset-liability matching strategy aimed at reducing interest rate volatility in the income statement.

Our profit after tax of $222m represents an annualised 24.5% ROTE with our tangible net asset value increasing by 12% to $2.04bn from $1.81bn at year-end.

Our balance sheet remains strong: reserves are struck conservatively; we have low levels of exposure to longer tail classes; we have a conservative investment portfolio; and our capital surplus is robust.

In 1H25, Insurance Contract Written Premium grew by 31% to $2.4bn, with strong contributions across our geographic and product segments. Despite rates being down 4% across our portfolio we have been able to deliver substantial underlying organic growth across our business, underpinned by strong rate adequacy.

The UK has shown positive performance in the first half of the year. While some of the portfolio is seeing rate pressure in a competitive environment, we remain disciplined where we are unable to achieve our required rate.

Portfolio Solutions has again seen substantial development from our new broker facilities and growth in existing ones. Property and Casualty saw stronger competition, particularly in property lines, but we were still able to achieve attractive underlying growth, notably in Casualty. Professional Lines saw good growth once again from our Cyber business, which, despite rate pressure, continues to perform well and Specialty saw good progress in a number of lines.

In the US, D&F property has seen some pressure on rate, although rate adequacy remains strong and we continue to make good progress in Cyber. We have reduced exposure in certain classes where rates are seen to be competitive (for example Financial Lines). We remain excited about the substantial growth opportunity in the US E&S market and continue to look for further opportunities to expand both product offerings and distribution capability.

Our Bermuda operations are benefitting from the addition of new underwriting capabilities and a broader base of clients and lines of business. From this base, we are confident that we can continue to build a strong and increasingly profitable operation, and we see plentiful opportunities to expand further.

APAC has once again seen strong growth as the business continues to develop its Property, Casualty, Reinsurance, and Specialty offerings. We continue to maintain a good pipeline of business and strong retention.

Looking ahead, we anticipate our performance to persist into the second half of the year. Rate adequacy remains robust and our presence in structural growth markets – combined with our diversified business model across product classes and geographies – positions us well to identify and capitalise on opportunities to allocate capital efficiently into profitable, expanding markets.

Neil Robertson

Group Chief Executive Officer